Weekly updatesJun 22, 2026

Weekly Market Outlook | June 15 - June 21, 2026

Edge Capital's weekly assessment of geopolitical risk, capital flows, protocol developments, and market structure across digital assets

Edge Capital

July 3, 2026

The wrapper is the asset.

Tokenized real world assets do not trade as pure exposure to the underlying security. A tokenized stock is not the stock. It is a claim on a wrapper, with its own issuer, custody chain, redemption process, liquidity profile, oracle, and collateral treatment.

This report answers two questions: what risks sit inside that wrapper, and when do those risks break the peg?

The answer is that depegs are not random. They occur when the market starts pricing one of five wrapper risks: credit, exit, rails, marks, or leverage. In calm markets, those risks are easy to ignore because the token trades close to the reference asset. Under stress, off hours, or size, they become the basis.

That basis is already visible. In one U.S. session, liquid mega caps traded within roughly 0.1 to 0.5% of the underlying. Thinner names traded at 1 to 2% premiums. The difference was not the stock. It was the cost of exit.

The second risk is credit. xStocks, Ondo, Binance bStocks, and Robinhood Stock Tokens are share backed today, but holders receive issuer claims, not registered ownership of the underlying shares. The rails are concentrated as well. Alpaca custodies roughly 94% of U.S. listed tokenized stocks, while Robinhood is building the main alternative on its own chain.

The third risk is time. Tokens trade continuously, but the underlying securities settle only on market days. Marks can freeze over weekends while secondary markets and liquidation engines keep running. Once these tokens are used as collateral, a small dislocation can become reflexive.

The clean failure case is when there is no liquid underlying to arbitrage against. PreStocks fell roughly 34 to 40% after its underlying share transfers were challenged. GBTC, China A/H pairs, and dual listed companies show the same lesson in different forms: backing matters, but redemption quality and arbitrage access determine the realized price.

The conclusion is simple: The peg is not the price. The price is the underlying asset adjusted for the wrapper’s weakest link.

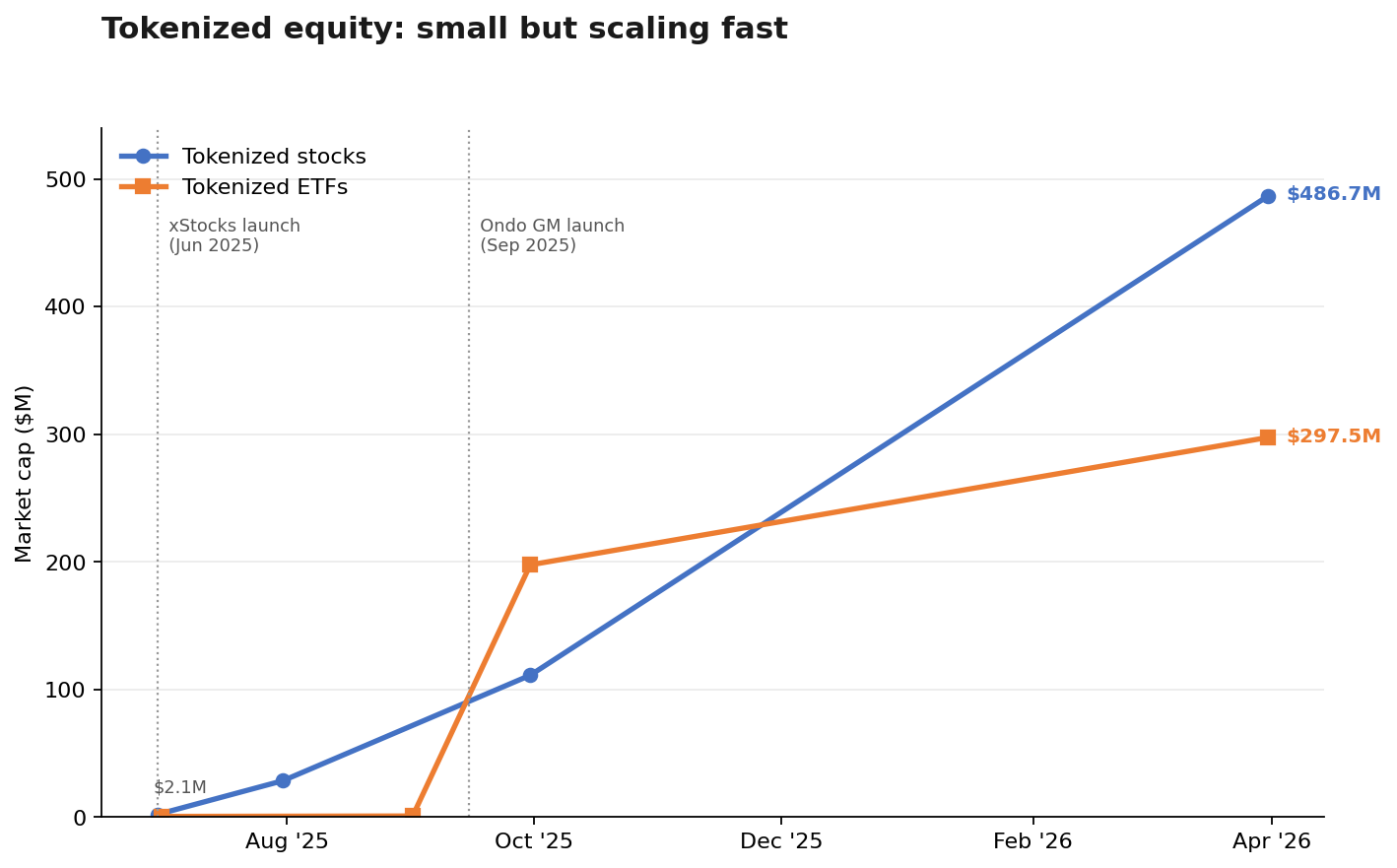

For most of their short life, tokenized equities were a curiosity: a familiar ticker on a blockchain. That has changed. The category is live across issuers, the largest exchanges, DeFi lending markets, and oracle networks. Allocators are increasingly offered these tokens as exposure and asked to accept them as collateral. The reason to underwrite them as instruments is that they are already being used as instruments.

The growth is the evidence. Tokenized stocks went from roughly $2mn in June 2025 to about $487mn by Q1 2026. RWA.xyz puts the market near $1.46bn by 29 June, led by Ondo at roughly $876mn (~57%) and xStocks at roughly $431mn (~28%).

Chart 1. Tokenized equity market capitalization growth.

Source: Edge Capital Research, CoinGecko 2026 RWA Report (Data as of 29 Jun, 2026)

Note: Markers are reported snapshots, not a daily series. The top five names trade under 1% of TradFi volume in the same tickers.

The field is crowding from every direction. Binance launched bStocks in June 2026: 1:1-backed tokens converted from brokerage positions and issued by group affiliate BTech Holdings. Robinhood moved its Stock Tokens onto its own chain on 1 July. Coinbase has outlined plans of its own. The market is still small against traditional equities, but no longer too small to matter to any book that touches DeFi. “Stocks on-chain” obscures more than it explains. The question that matters is what risks you actually hold.

Treat a tokenized stock as its own instrument. It may reference Apple or the S&P 500. But it carries its own issuer, custody stack, redemption process, oracle, venue depth, and collateral treatment. The relevant price is the stock adjusted for all of that. The institutional question is not whether the token tracks the equity in calm conditions. It is what happens when the arbitrage channel narrows or closes.

Three structures define the market, with different peg mechanisms and different failure modes.

Table 1. Tokenized equity wrapper taxonomy.

| Structure | Examples | Peg mechanism | Main risk |

|---|---|---|---|

| Fully backed wrapper | xStocks, Ondo, Binance bStocks, Robinhood | Mint / redeem or 1:1 convert against the underlying | Redemption friction, issuer credit, liquidity |

| Synthetic wrapper | Mirror mAssets (historical) | Oracle plus collateral | Collateral-system failure |

| Private / SPV wrapper | PreStocks, OpenAI / SpaceX SPV tokens | SPV or contractual exposure | No liquid underlying; legal and valuation risk |

Source: Edge Capital Research

Fully backed wrappers hold real collateral and lean on redemption to stay near fair value. Synthetic wrappers hold no shares. They depend on oracle marks and system solvency; Mirror’s mAssets, which failed with Terra in 2022, remain the archetype. Private and SPV wrappers have the weakest peg. With no liquid underlying and no open arbitrage, the token trades as a scarcity claim. Every fully backed wrapper carries the same five risks. The peg is where they show.

Start with the legal claim, because none of the leaders hands you the share. xStocks are debt of a Jersey SPV with a claim on a collateral pool. Ondo tokens are claims on a BVI issuer with permissioned transfer. bStocks are a credit claim on BTech Holdings, an Abu Dhabi SPV. Robinhood Stock Tokens are tokenized debt of Robinhood Assets (Jersey) Limited. In every case the holder owns issuer credit wrapped around economic exposure, not registered ownership.

Table 2. The claim, the backing, and the door: issuer comparison.

| Issuer | Legal claim | Backing today | Primary access |

|---|---|---|---|

| xStocks (Backed) | Debt claim on a Jersey-SPV collateral pool | 100%+ in actual shares per live proof-of-reserves; substitution permitted | Onboarded primary users; market-day mint and redeem; retail exits via CEX / DEX |

| Ondo Global Markets | Token claim on a BVI issuer; permissioned transfer | Underlying held via broker custody | KYC’d qualified non-US investors; weekend mint / redeem added 25 June for six names, session-capped; ~400 other listings market days only |

| Binance bStocks | Credit claim on BTech Holdings (ADGM SPV) | 1:1 against converted brokerage positions | Binance brokerage users (non-US); 1:1 convert; underlying settles market days |

| Robinhood Stock Tokens | Tokenized debt of Robinhood Assets (Jersey) Ltd | Shares in Robinhood’s own custody | Robinhood Wallet, 120+ countries; U.S. excluded |

Source: Edge Capital Research, issuer documentation and announcements

Backing is strong today and must be monitored, not assumed. xStocks’ live proof-of-reserves showed every token at or above 100% in the actual underlying shares as of 29 June. Yet the documentation permits substitute or cash collateral. So the correct statement is precise: verifiably share-backed today, with substitution and issuer-credit risk retained. Transferability splits the group as well. xStocks moves permissionlessly; Ondo transfers are permissioned. That trades secondary-market reach against issuer control.

Dividends are part of the same claim question. xStocks and Ondo reinvest them through a rising multiplier, net of 30% U.S. withholding. Those tokens drift above the ticker by design. Robinhood’s earlier European tokens paid dividends in-app as cash. The analytical consequence is the same either way: measure premium and discount against accrued value, not the raw exchange quote, or a total-return wrapper will read as permanently rich.

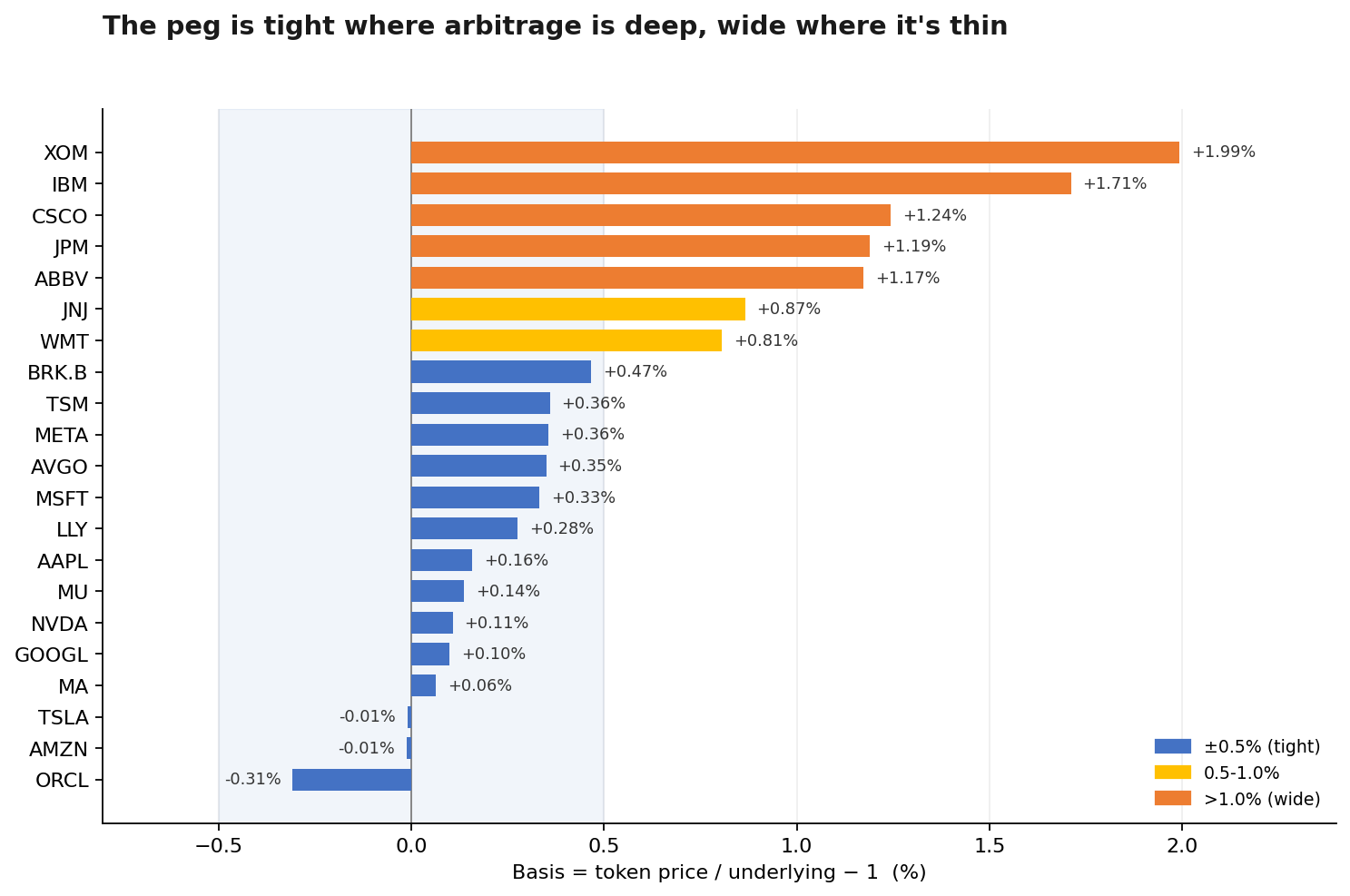

The basis is the market’s answer, printed daily. In the same U.S. session, Nvidia, Apple, Google, Amazon, Tesla, and Microsoft traded within roughly 0.1–0.5% of the underlying. XOM, IBM, CSCO, JPM, and ABBV ran 1–2% premiums. Observed in one window, that spread isolates liquidity: the basis prices exit access, not time of day.

Exhibit 5a. Basis by name, single U.S. session.

Source: Edge Capital Research, CoinMarketCap RWA (Data as of 29 Jun, 2026, ~4pm ET)

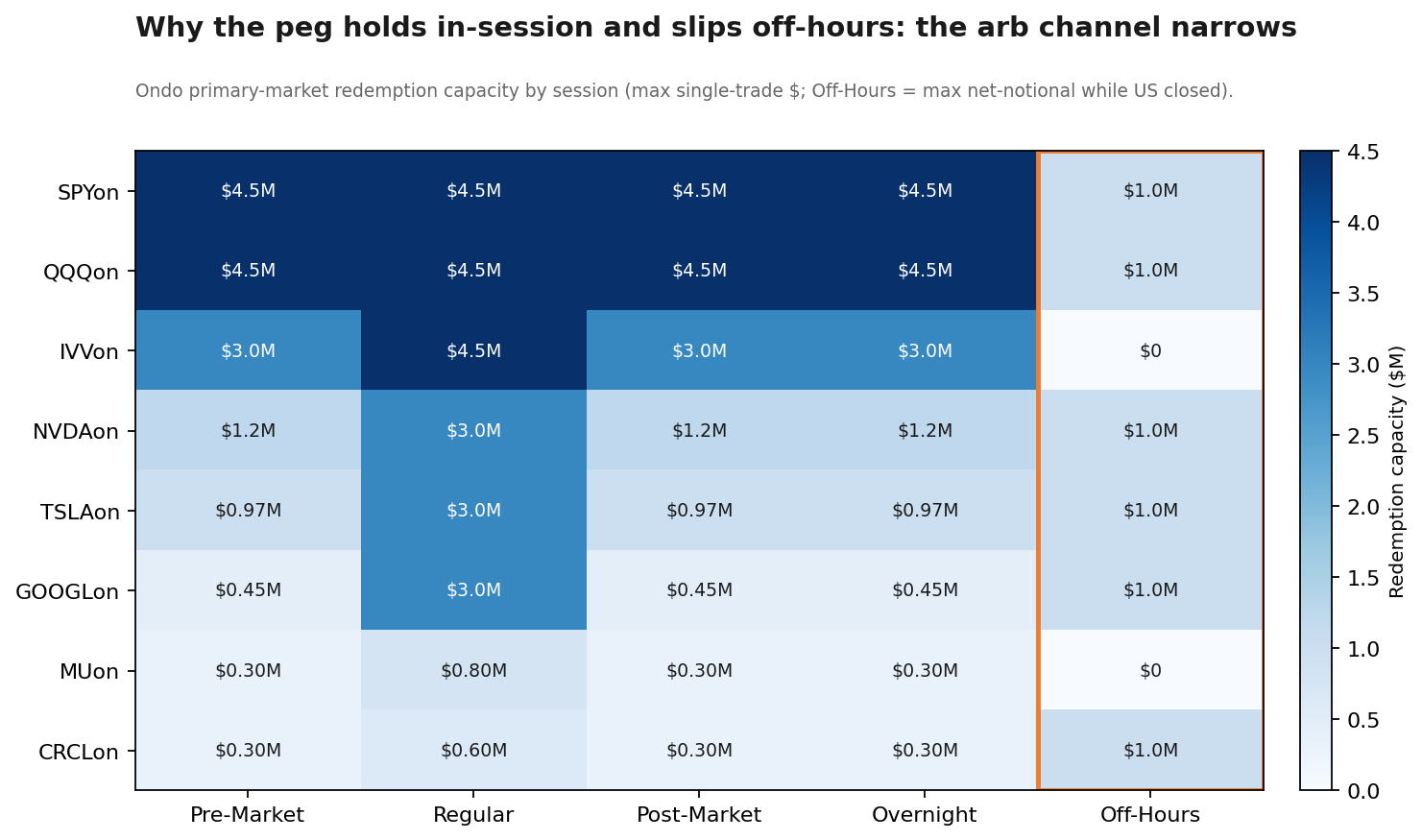

Ondo’s session data supplies the mechanism. In regular hours, single-trade minting and redemption runs roughly $3–4.5mn for the marquee names and is repeatable. That is deep enough to arbitrage the basis flat. On 25 June, Ondo extended minting and redemption into weekends and U.S. holidays for six names (SPYon, QQQon, CRCLon, NVDAon, TSLAon, GOOGLon) on Ethereum and BNB Chain, subject to session caps near $1mn of net notional. Its remaining listings, more than 400 names, mint and redeem on market days only. The underlying still settles on market days. So weekend execution runs on pre-positioned inventory, and the caps are the measure of that inventory.

Exhibit 5b. Ondo primary-market capacity by session.

Source: Edge Capital Research, Ondo (status.ondo.finance) (Data as of 29 Jun, 2026)

Note: Off-Hours means weekends and U.S. holidays. Capacity there is capped near $1mn net for the six names with weekend mint / redeem, and zero for every other listing. The channel narrows exactly when equities close.

So size clears through the primary market, not the DEX. On-chain pools handle retail flow and price discovery. An institutional exit depends on issuer capacity, and that capacity narrows exactly when the equity market closes. The off-hours column is depeg risk, quoted in advance.

Beneath nominally separate issuers sits one broker. Alpaca Securities, a U.S. self-clearing FINRA member, custodies roughly 94% of U.S.-listed tokenized stocks. It sources and holds the underlying for xStocks and Ondo alike. Binance’s bStocks are not the exception. The securities product behind them routes through Alpaca as well, with group entity Nest Trading as introducing broker while Alpaca executes, clears, settles, and custodies. Binance also holds a minority stake in Alpaca.

The dependency is documented, not inferred. Binance’s own terms provide for converting every client position to an alternative broker-dealer if the Alpaca relationship ends. If the broker layer is impaired or withdraws support, much of the category is affected at once: correlated operational and redemption risk that belongs inside the wrapper price.

The alternative is being built in public. On 1 July 2026, Robinhood moved its Stock Tokens onto Robinhood Chain, its own Arbitrum-Orbit Layer 2 with ETH gas, Ethereum data availability, and a sequencer Robinhood runs for compliance and order routing. Tokens are live through Robinhood Wallet in more than 120 countries, the U.S. excluded. Robinhood self-clears through Robinhood Securities: the one large issuer that does not sit on Alpaca.

It now owns clearing, issuance, distribution, and settlement end to end. It is wired into open DeFi rails through Uniswap and Pleiades liquidity, 0x request-for-quote, Chainlink oracles, and BitGo. Against a market where one broker holds most of the collateral, this is the first credible vertically integrated alternative.

The wrapper itself is familiar. Stock Tokens are tokenized debt of Robinhood Assets (Jersey) Limited. Each is backed by a share in Robinhood’s own custody, but the holder receives economic exposure only, with no rights in or against the underlying issuer. A token withdrawn to self-custody carries neither SIPC nor FDIC protection. Robinhood’s separate OpenAI and SpaceX tokens, SPV-wrapped private exposure that OpenAI publicly disavowed, sit a tier lower and should not be confused with the share-backed names.

Most important, the two-clock problem survives vertical integration. The underlying still trades only in U.S. hours. Off-hours, the price is held by Robinhood and its market makers carrying inventory while the spread widens. That is the same mechanic xStocks runs. Owning the rails removes the shared broker. It does not remove the wrapper basis, the issuer claim, or the weekend gap. It does signal the direction of travel: issuers internalizing the stack to escape the single-broker chokepoint, while the risks an allocator must check stay the same.

The marks behind these tokens run on the equity clock. Chainlink’s feeds draw from U.S. exchanges and stop discovering price when those exchanges close. Yet the tokens keep trading on-chain and liquidation engines keep running. The mark freezes while the market keeps moving.

Table 3. Behavior when the U.S. market is closed.

| Product | Mark source | Feed type | Behavior when the U.S. market is closed |

|---|---|---|---|

| Ondo | Chainlink, from U.S. exchange data | Total-return (accrued NAV) | Mark freezes at last print; weekend minting and redemption for six names is capped and priced off models and quotes rather than live discovery; the DEX price can drift from the frozen NAV |

| xStocks | Chainlink custom oracle, with stale-price detection | Price plus daily multiplier | Token keeps trading on Solana and Ethereum against a stale mark; Kamino liquidations run against that mark; quotes far from last close are rejected by oracle bounds |

| Robinhood | Chainlink on Robinhood Chain; issuer and market-maker quotes | Price | Token trades continuously on Robinhood Chain while the issuer and its market makers carry inventory and the spread widens |

Source: Edge Capital Research, Chainlink, Ondo, xStocks, Robinhood

The risk is not oracle design. Ondo’s feeds add corporate-action freezes and stale-price bounds, and the ENLVon pause shows issuer halts are live tools. The risk is the gap between a frozen mark and a live secondary market. Over a weekend the token can drift from last NAV. A wrong print or a sentiment move can trigger liquidations against a stale price that cannot be arbitraged back until equities reopen.

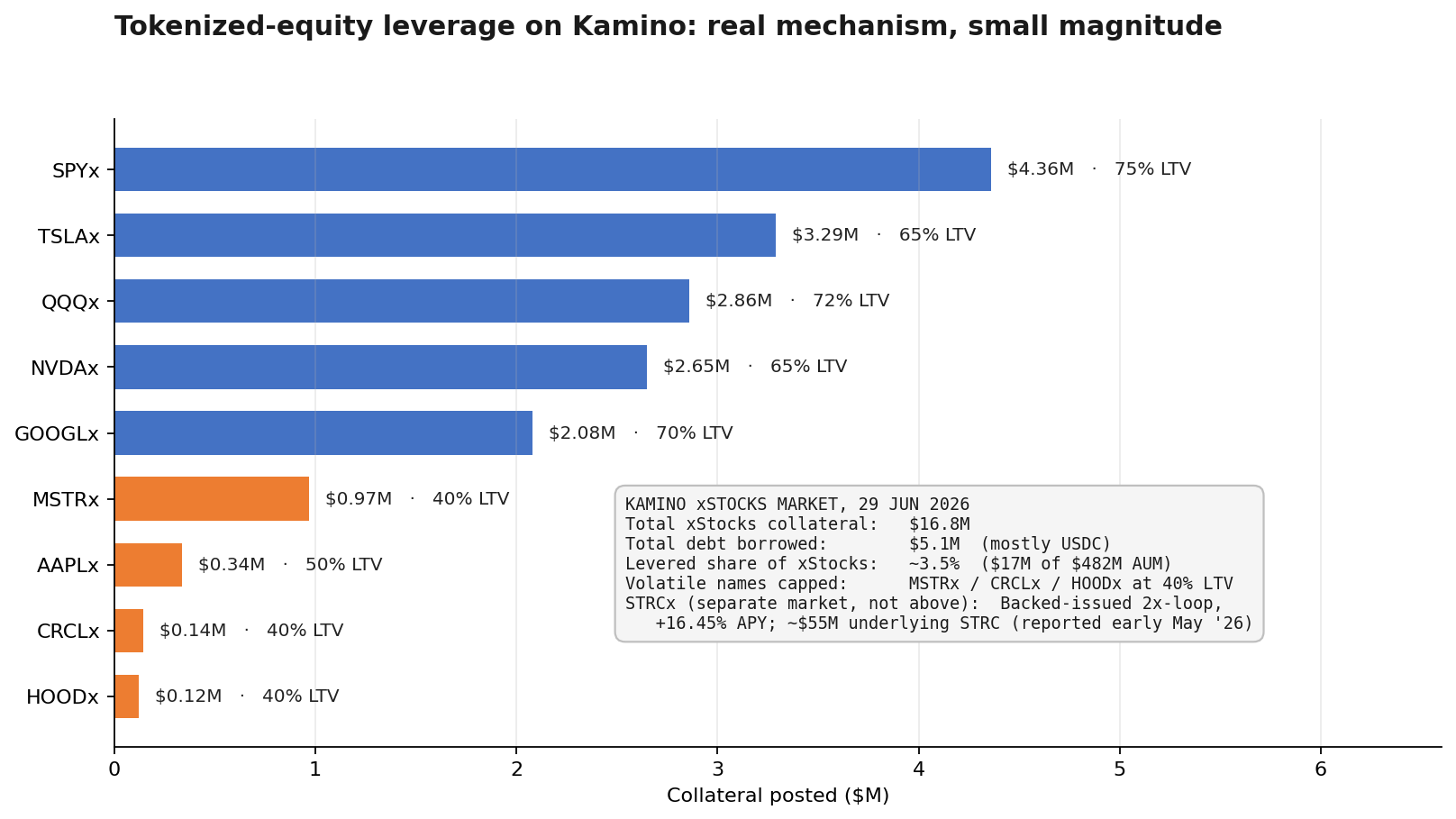

Everything above is a return question until the token is posted as collateral. Then it becomes a solvency question. On Kamino, xStocks back roughly $16.8mn of collateral against $5.1mn of debt. That is about 3.5% of xStocks AUM levered through the venue, concentrated in liquid names at conservative-to-moderate LTVs.

Exhibit 6. Kamino xStocks debt vs collateral.

Source: Edge Capital Research, Kamino (Data as of 29 Jun, 2026)

Note: The contagion mechanism is real, but live exposure is small: roughly $5mn of debt against $17mn of collateral, about 3.5% of xStocks AUM. On-chain DEX depth is thin, near $0.3–1mn per name, so the risk is latent, not acute.

The exposure is real but not yet acute, and it runs wider than one venue. Tokenized equities also appear as collateral on Morpho’s Ethereum markets at sizes too small to break out, so Kamino remains the only venue we can size precisely. The pocket to watch is STRCx, Backed’s tokenized Strategy preferred. It trades in its own dedicated Kamino market with one-click looping and a multiply APY near 16%: the most reflexive corner of the set, separate from the figures above.

PreStocks is the clean failure case. It tokenized Anthropic and OpenAI exposure. Both companies declared the underlying share transfers void, and the tokens fell roughly 34–40% once the claim was challenged. The product had implied an Anthropic valuation near $1.3tn against roughly $23mn of disclosed assets, and the promised attestations never appeared. With no liquid underlying, there was never a peg to defend, only a legal claim with crypto liquidity around it.

Traditional finance already ran this experiment. GBTC held real bitcoin but lacked open redemption. It swung from deep premium to deep discount until ETF conversion restored the channel. China A/H pairs hold identical exposure at persistent gaps under capital controls. Dual-listed companies stayed off parity for years. Backing matters, but redemption quality and arbitrage access set the realized basis.

Underwriting a tokenized asset means checking five risks:

1. Credit. Whose claim you hold: which SPV, what backing evidence, what substitution rights.

2. Exit. Who can redeem, when, at what size and fee, and what happens on a weekend.

3. Rails. Which broker, custodian, and chain sit underneath, and how concentrated they are.

4. Marks. Whether the reference is a raw price, a total-return feed, a token print, or issuer NAV, and how it behaves when equities are closed.

5. Leverage. Whether the token is posted as collateral, at what LTV, against what liquidation logic and DEX depth.

The market will likely bifurcate by structure. Products with clear backing, low-cost redemption, robust oracle design, and deep primary capacity should consolidate institutional flow. Wrappers without liquid underlying markets, direct redemption, or verifiable backing will trade like structured claims or sentiment instruments. The long-run direction is fewer wrapper layers: native issuance, broker-dealer and transfer-agent rails, regulated tokenized-securities infrastructure, and, as Robinhood shows, issuers who own the stack.

None of it removes the residual. As long as the token trades continuously and the underlying does not, an off-hours basis remains, and it belongs in the price. Tokenized equities are useful instruments. Their risks are real, and they are measurable. A depeg is never a surprise. It is the wrapper’s risk, finally quoted.

Disclaimer

This communication is for information purposes only and is not an advertisement, an offer, invitation or a solicitation to buy or sell securities or investment products, an official confirmation of any kind and is not intended as investment advice or recommendation. Before making an investment decision, investors should ensure they have sufficient information to ascertain the legal, financial, tax and regulatory consequences of an investment to enable them to make an informed investment decision. The information in this communication is subject to change without notice. No warranty is made as to the completeness or accuracy of the information contained in this communication, and the information in this email may be erroneous, invalid and/or unsubstantiated. The sender therefore does not accept liability for any errors, omissions or adverse consequences in the contents of this message which arise as a result of e-mail transmission or for any other reason.

The performance and value of any financial product may fluctuate and may be subject to sudden and large movements that could result in a loss equal to or in excess of the amount invested. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. The presented figures are based on estimates, assumptions, models and third-party data, any or all of which may prove to be inaccurate.