Weekly updatesJun 08, 2026

Weekly Market Outlook | June 1 - June 7, 2026

Edge Capital's weekly assessment of geopolitical risk, capital flows, protocol developments, and market structure across digital assets

Edge Capital | March 2026

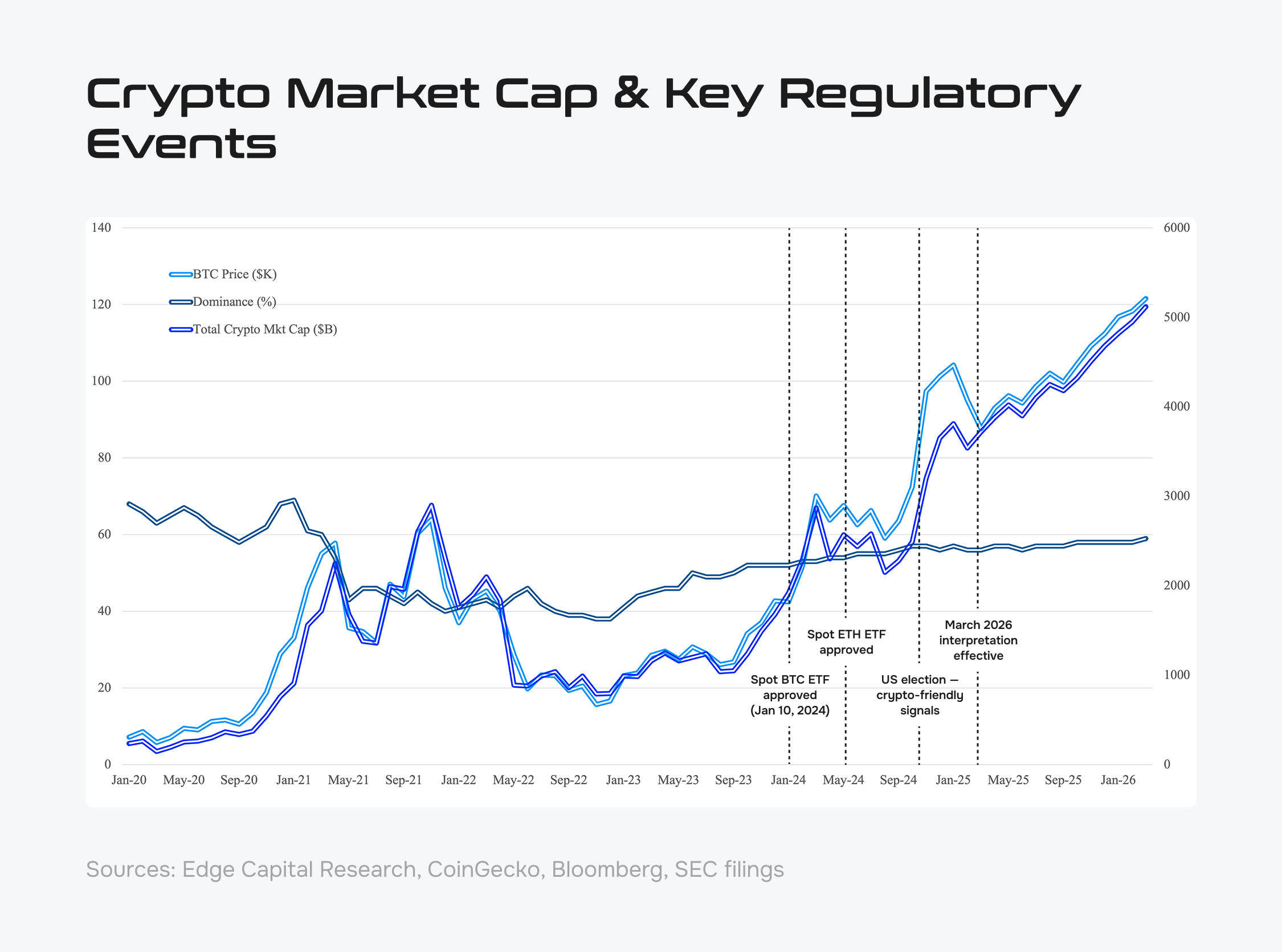

On March 23, 2026, the SEC and CFTC jointly published a landmark interpretation in the Federal Register establishing the first comprehensive federal taxonomy for crypto assets. In our view, this is the most consequential regulatory development for digital assets since the passage of the GENIUS Act — and the most structurally significant for institutional capital allocation since the approval of spot Bitcoin ETFs in January 2024.

The interpretation does not introduce new legislation. It does something more durable: it replaces more than a decade of case-by-case enforcement with systematic, prospective classification by characteristics and function. Every digital asset now has a regulatory home. The implications for how institutions participate in this market are structural, and we believe they are lasting.

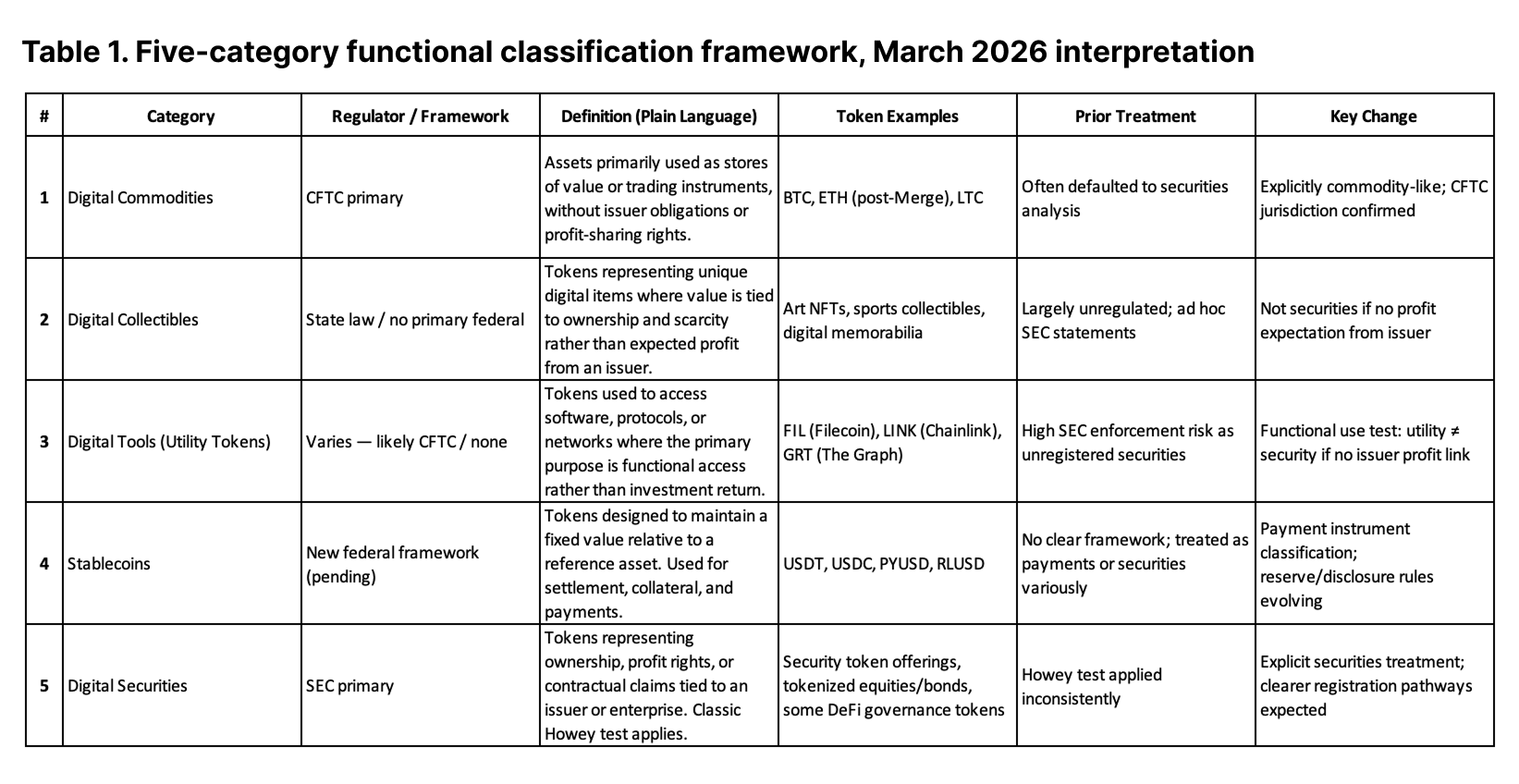

The interpretation introduces five classifications, each carrying distinct treatment under federal law.

Digital Commodities are assets whose value derives from the programmatic operation of a functional blockchain network and from supply and demand — not from the managerial efforts of a development team. These are explicitly excluded from securities treatment. Sixteen assets received formal classification: Bitcoin, Ether, Solana, XRP, Cardano, Avalanche, Chainlink, Dogecoin, Litecoin, Polkadot, Shiba Inu, Stellar, Tezos, Hedera, Bitcoin Cash, and Aptos.

Digital Collectibles cover assets designed to be collected or used — artwork, music, trading cards, in-game items, and meme coins. Value derives from supply, demand, and cultural significance rather than managerial effort, placing them outside securities treatment. Assets in this category may transition to digital commodity status if they gain functional utility within a blockchain network.

Digital Tools are assets that perform a practical function: memberships, access credentials, tickets, and identity instruments. ENS domain names are cited as an example. These are not securities.

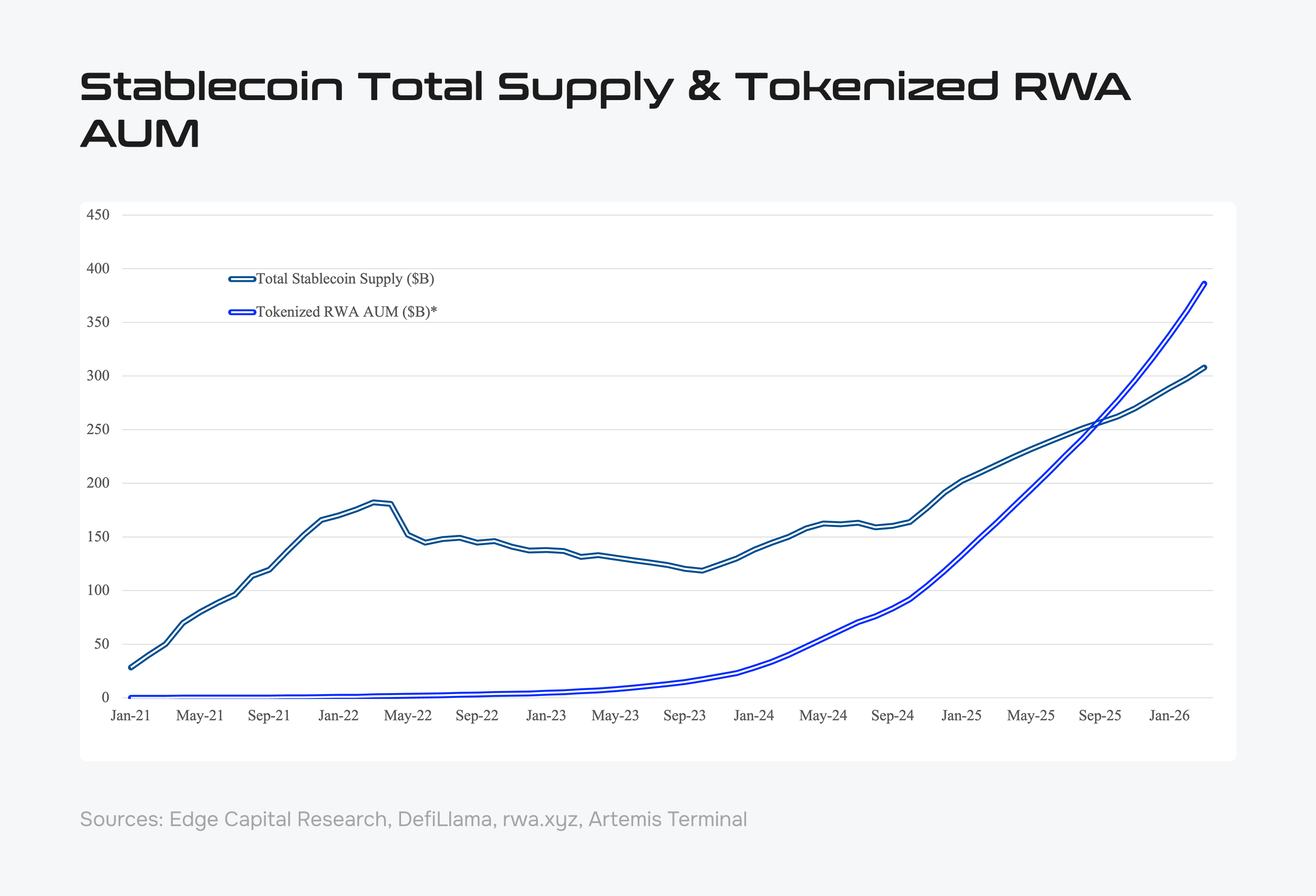

Stablecoins issued under the GENIUS Act by permitted issuers are excluded from securities treatment by statute. Stablecoins outside that definition remain subject to case-by-case evaluation — an area we address below.

Digital Securities are traditional financial instruments — stocks, bonds, investment contracts — represented on a blockchain. These remain fully subject to existing securities law.

The methodology shift is, in our view, as significant as the taxonomy itself.

The SEC's prior approach applied the Howey test retroactively — asset by asset. Institutional capital that cannot operate without a defensible analytical framework did not participate. That constraint is now removed.

The new interpretation also introduces a formal mechanism through which investment contract status terminates — either when the issuer fulfills its commitments or when the project achieves sufficient decentralization. The asset then moves to non-security status. Two additional protections sharpen this: only representations made by or authorized by the issuer count toward securities analysis, and post-sale issuer statements cannot retroactively reclassify a prior transaction. Both eliminate vectors of legal risk that previously had no resolution.

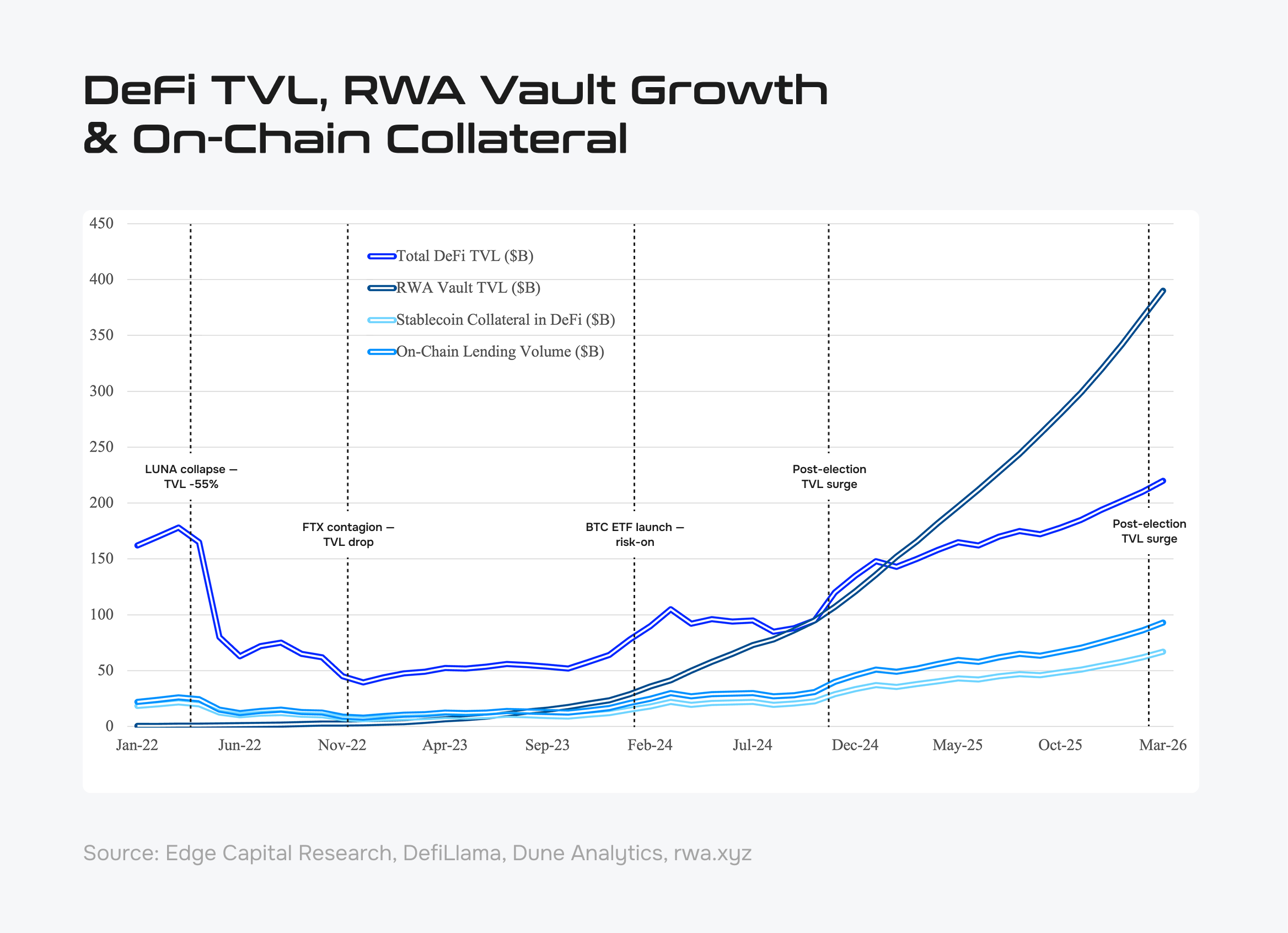

The interpretation resolves long-standing ambiguity around core protocol activities that institutional participants have treated as open legal questions — and in doing so, substantially expands the investable perimeter.

Protocol staking — whether solo, delegated, or pooled — is not a securities transaction. Rewards derive from protocol mechanics, not from managerial efforts. Liquid staking tokens such as stETH and rETH, representing deposited non-security assets, are not securities. They evidence ownership of the underlying asset, and that ownership transfer is unambiguous under the new framework.

Wrapping a non-security asset does not create a security. Wrapped tokens are redeemable receipts for deposited assets; wrapping providers are explicitly prohibited from lending, pledging, or rehypothecating the underlying. Certain airdrops that do not involve an investment of money under Howey also fall outside securities treatment.

For institutions with exposure to decentralized infrastructure, this removes a category of regulatory risk that has constrained participation for years. The compliance framework for DeFi is now defined rather than inferred.

Regulatory clarity and market infrastructure are now moving in the same direction — and the sequencing matters.

Concurrent with the taxonomy publication, the NYSE removed its 25,000-contract position limits on crypto ETF options. In our view, this is not coincidental. Position limits are not expanded on instruments tied to assets with unresolved regulatory status. The NYSE's decision reflects a market-structure judgment that the underlying framework is sufficiently settled to support institutional-scale activity.

The CFTC's concurrent guidance confirms that non-security crypto assets may qualify as commodities under the Commodity Exchange Act. Between the SEC taxonomy and the CFTC confirmation, jurisdictional ambiguity — where neither regulator claimed clear authority over the full asset class — no longer exists.

The interpretation does not resolve everything, and precision on that point matters for risk assessment.

Stablecoins outside the GENIUS Act definition remain subject to case-by-case evaluation. Reserve requirements, disclosure obligations, and oversight frameworks for that broader category are still evolving. DeFi protocols without an identifiable issuer present unresolved questions — the traditional securities analysis presupposes a party making representations, and fully decentralized systems do not always have one.

The relevant observation for institutional participants is this: risk has not disappeared. What has changed is that risk is now measurable. Compliance teams can draw boundaries. Investment committees can document their analysis. The shift from unknown risk to quantifiable risk is precisely what moves institutional capital — and it is a more durable catalyst than price.

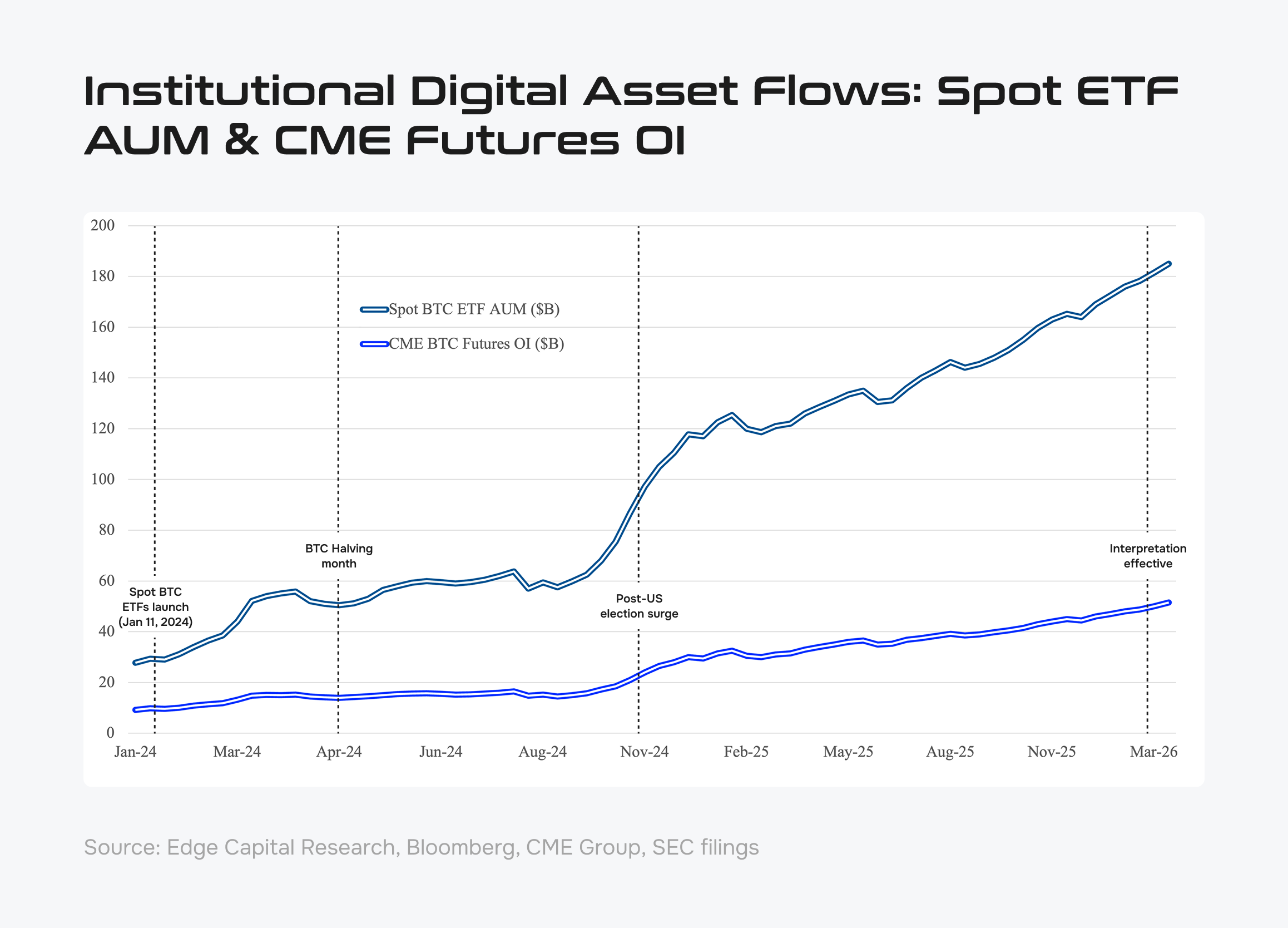

The leading indicator of institutional capital deployment is not price. It is pipeline.

Since the passage of the GENIUS Act and the broader shift in regulatory posture, we have observed a measurable increase in institutional engagement: compliance frameworks under review, allocators conducting due diligence on custody infrastructure, counterparties initiating coverage of assets they had previously avoided. These conversations precede capital deployment by quarters, not weeks.

We do not anticipate dramatic capital reallocation in the near term. Regulatory guidance takes time to move through compliance frameworks, investment committees, and board mandates. But the direction is unambiguous, and the structural change is already in place. We will be watching spot ETF flow data, prime brokerage onboarding activity, and open interest across regulated venues as confirmation signals.

The opportunity set is expanding — not because the technology changed, but because the regulatory architecture has caught up to it. For participants with the infrastructure, the relationships, and the analytical framework to operate within it, the conditions are now in place.

For treasury managers, the framework provides a defined basis for determining which assets are eligible under internal investment policies — without requiring external legal opinions for each position.

For funds and allocators, it simplifies product structuring across token categories and removes the ambiguity that previously required conservative assumptions to protect against enforcement risk.

For banks, custodians, and prime brokers, it establishes how digital assets should be treated for reporting, capital, and risk purposes — accelerating the buildout of institutional-grade service infrastructure.

For credit and derivatives markets, it expands the range of assets that can be used as collateral, with consistent classification enabling consistent risk management at scale.

The interpretation does not compel capital into the market. It makes participation possible on terms that regulated entities can defend — which is, in practice, the more important condition.

Disclaimer: This communication is for information purposes only and is not an advertisement, an offer, invitation or a solicitation to buy or sell securities or investment products, an official confirmation of any kind and is not intended as investment advice or recommendation. Before making an investment decision, investors should ensure they have sufficient information to ascertain the legal, financial, tax and regulatory consequences of an investment to enable them to make an informed investment decision. The information in this communication is subject to change without notice. No warranty is made as to the completeness or accuracy of the information contained in this communication, and the information in this email may be erroneous, invalid and/or unsubstantiated. The sender therefore does not accept liability for any errors, omissions or adverse consequences in the contents of this message which arise as a result of e-mail transmission or for any other reason. The performance and value of any financial product may fluctuate and may be subject to sudden and large movements that could result in a loss equal to or in excess of the amount invested. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. The presented figures are based on estimates, assumptions, models and third-party data, any or all of which may prove to be inaccurate.