Weekly updatesApr 13, 2026

Weekly Market Outlook | Apr 6 - 12, 2026

Edge Capital's weekly assessment of geopolitical risk, capital flows, protocol developments, and market structure across digital assets

Stablecoins have, in our view, become the most established and economically relevant application in digital assets. Their primary function is payments: efficient, borderless, and low-cost value transfer. By operating outside correspondent banking networks, stablecoins materially reduce settlement times to seconds and transaction costs to cents, enabling near real time business to business, peer to peer, and cross border payments.

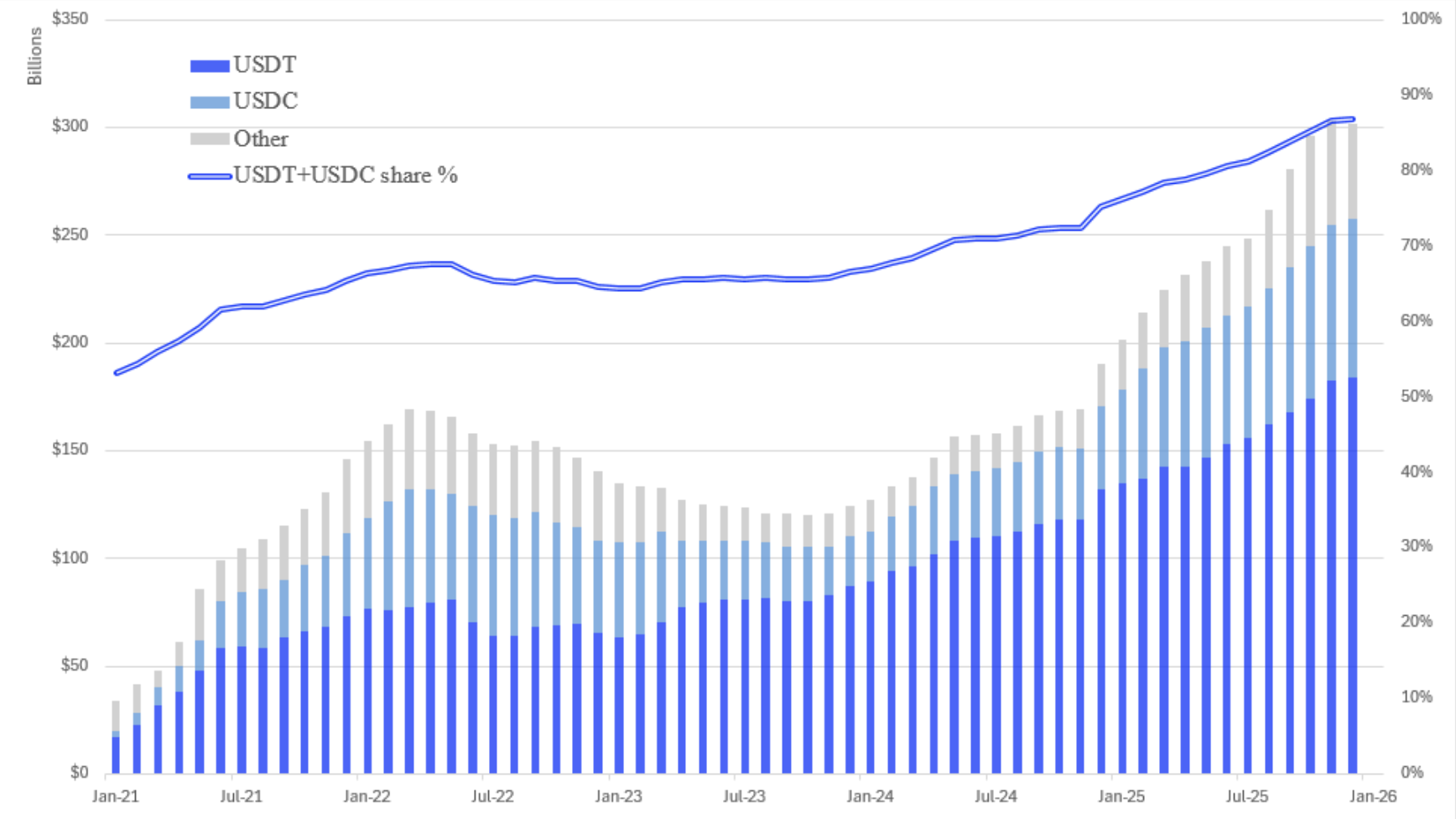

Regulation is now structurally reshaping the stablecoin market. In the U.S., the GENIUS Act provides a clear path for institutional adoption by defining payment stablecoins as fully reserved transactional instruments, backed one for one by cash and short dated U.S. Treasuries. This framework embeds stablecoins within regulated payment and treasury systems, while prohibiting issuers from distributing underlying reserve yield (3% from money-markets) directly to end users.

As a result, yield ceases to be a source of differentiation at the payment layer, and competition shifts away from balance sheet economics toward structure and distribution. We expect market share to migrate towards issuers that can pair compliant stablecoins with adjacent financial services, such as cash-management wrappers, integrated treasury dashboards, and credit solutions without breaching reserve and disclosure rules.

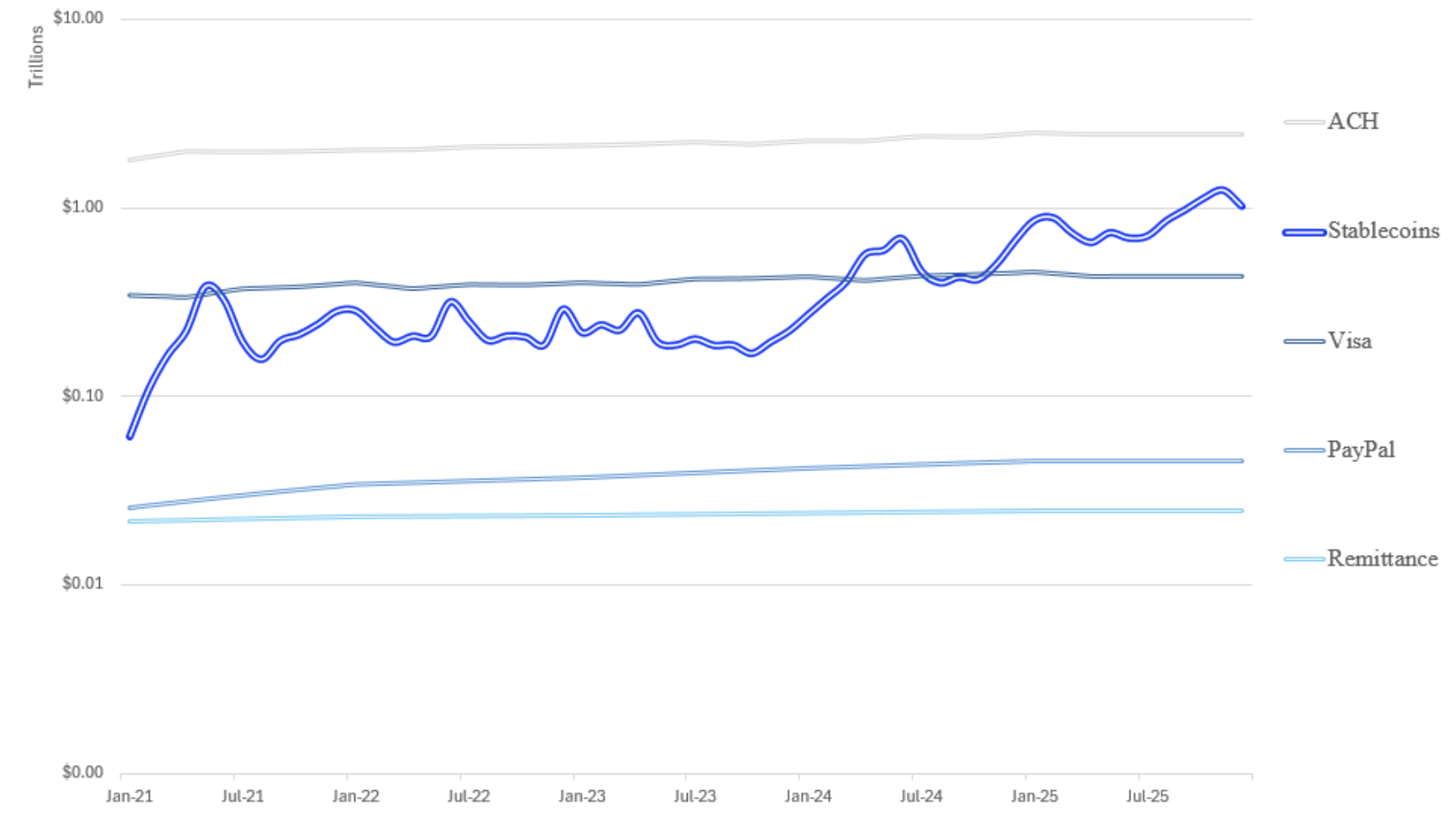

Stablecoin transaction volumes have scaled rapidly and now operate at multi-trillion-dollar annualized levels. On a relative basis, they are comparable in magnitude to large global payment networks and exceed traditional remittance and digital payment rails. This comparison uses annualized transaction value to illustrate settlement scale and does not represent a direct comparison with consumer-facing payment volumes.

The trajectory reflects a rising baseline with intermittent spikes, consistent with a settlement network that is expanding in both scale and frequency of use. Taken together, this supports the view that stablecoins are no longer a niche crypto instrument, but a meaningful settlement mechanism within global payments activity.

Disclaimer

This communication is for information purposes only and is not an advertisement, an offer, invitation or a solicitation to buy or sell securities or investment products, an official confirmation of any kind and is not intended as investment advice or recommendation. Before making an investment decision, investors should ensure they have sufficient information to ascertain the legal, financial, tax and regulatory consequences of an investment to enable them to make an informed investment decision. The information in this communication is subject to change without notice. No warranty is made as to the completeness or accuracy of the information contained in this communication, and the information in this email may be erroneous, invalid and/or unsubstantiated. The sender therefore does not accept liability for any errors, omissions or adverse consequences in the contents of this message which arise as a result of e-mail transmission or for any other reason.

The performance and value of any financial product may fluctuate and may be subject to sudden and large movements that could result in a loss equal to or in excess of the amount invested. Past performance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. The presented figures is based on estimates, assumptions, models and third-party data, any or all of which may prove to be inaccurate.